PE Value Creation Newsletter: Issue 1

Josh Miramant

Blue Orange Digital

PE Value Creation Newsletter

Issue 1 · April 2026

Welcome to the inaugural issue of the PE Value Creation Newsletter from Blue Orange Digital. Each issue brings you data-driven intelligence on the forces reshaping private equity returns, from macroeconomic signals and LP sentiment to AI infrastructure and operational value creation levers.

In This Issue

01 Market Intelligence — The Rate Pivot That Is Not Coming: What 40% Means for PE in 2026

02 Data Spotlight — The DPI Crisis: LP Patience Has Expired

03 Deal Flow — $904B in Deal Flow: Where Prediction Markets Say It Goes Next

04 Blueprint Corner — AI Is a PE Value Creation Mandate: Your Data Infrastructure Decides

Market Intelligence

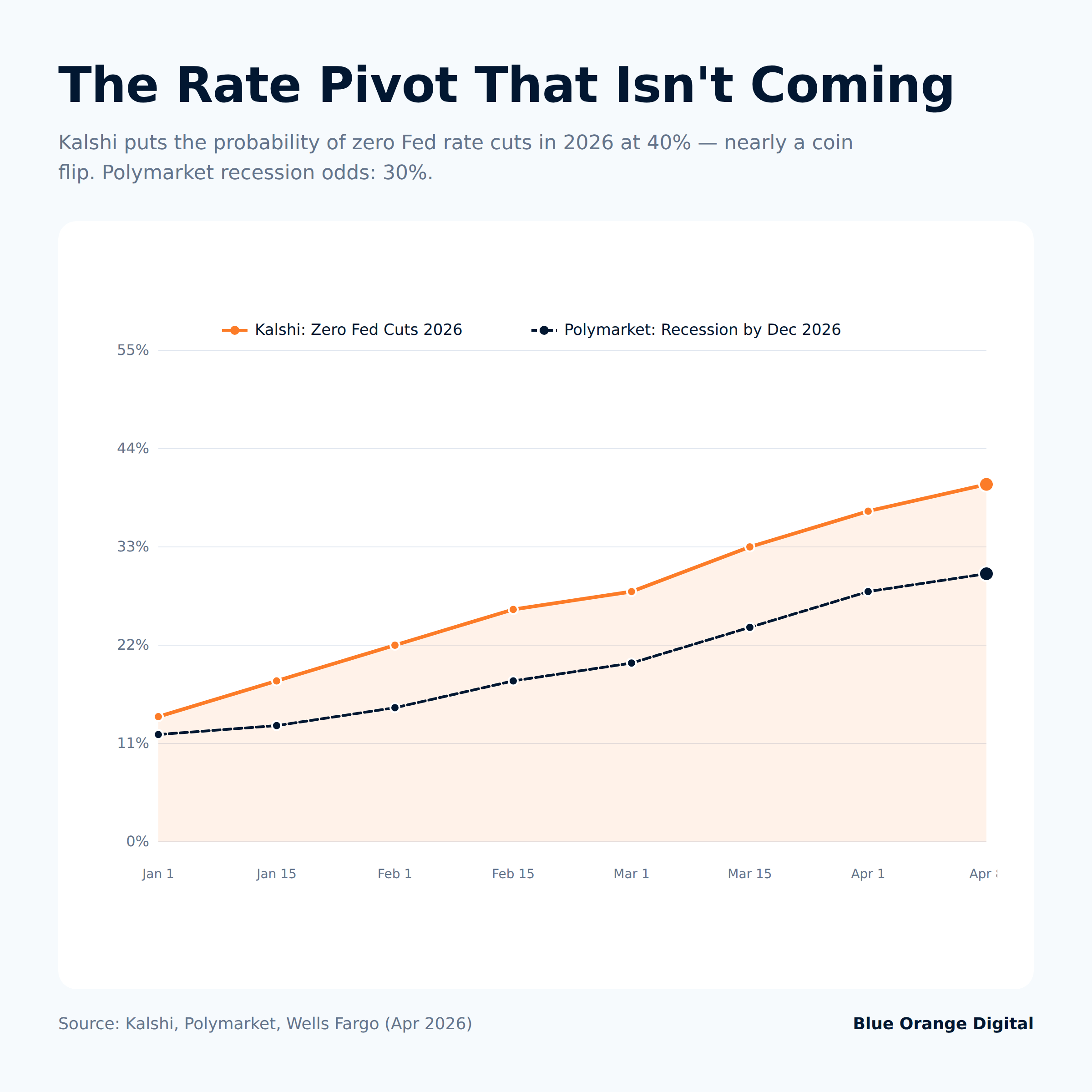

The Rate Pivot That Isn't Coming: What 40% Means for PE in 2026

Kalshi prediction market: 40% probability of zero Fed rate cuts in 2026

Wells Fargo made it official on April 6th: they are removing all 2026 Federal Reserve rate cuts from their baseline forecast. This is not a fringe view.

Think about what that number actually means. Four in ten market participants who put real money behind their convictions believe the Fed will not move once this year. That is not a tail risk. That is a near coin flip, and it is leaning the wrong way for every GP who underwrote a deal on a “rates-down-by-Q3” thesis.

The current Fed funds rate sits at 3.50–3.75%. For firms that loaded up on leverage at 2021 valuations with the expectation that rate relief was one or two quarters away, the math has grown harder with each passing quarter. Hold periods extend. LP distributions stay thin. The pressure compounds.

The firms navigating this environment without bleeding are the ones that stopped waiting for the rate environment to rescue them. They rewrote their value creation playbooks to operate independently of rate movement.

What that looks like in practice: operational improvement as the primary lever, not multiple expansion. Portfolio companies that can demonstrate genuine margin improvement, organic revenue growth, and working capital discipline will attract buyers and generate exits in any rate environment.

There is a harder question embedded in the 40% figure. If zero cuts is a genuine possibility, what does that mean for the $1.3 trillion in dry powder sitting on the sidelines (much of it from 2022–23 vintages that need to deploy)? GPs cannot sit out indefinitely. The clock on fund deployment timelines keeps running regardless of what the Fed does.

Citigroup still sees cuts coming, eventually. The April employment data gave the soft-landing camp something to work with: March nonfarm payrolls came in at 178,000 against a 59,000 expectation, and unemployment dipped to 4.3%. The recession case is not proven. But Polymarket still puts it at 30% by year-end, and Kalshi’s recession odds hit 37% briefly before settling at 28%.

The gap between “no recession” and “confident recovery” is exactly where deal-making gets uncomfortable. At 28–30% recession probability, sponsors cannot underwrite to a downside scenario and generate attractive returns. They also cannot ignore a nearly-one-in-three probability that conditions get significantly worse.

Build for the rate environment you have, not the one you expected.

Sources: Kalshi · Wells Fargo via TheStreet · Polymarket

Data Spotlight

The DPI Crisis: LP Patience Has Expired

6%

Current DPI as share of PE AUM

vs. 16% historical average

$240B

Secondaries volume in 2025

+48% year-over-year, all-time record

The private equity industry has a liquidity problem, and the data is unambiguous about how serious it has become.

In the 12 months ended June 2025, DPI as a share of PE assets under management stood at 6%. The historical average is 16%. That gap (10 percentage points of missing distributions relative to what LPs have come to expect) represents trillions of dollars in capital that has not come back to investors.

The five-year rolling DPI figure hit its lowest recorded level in June 2025. McKinsey’s Global Private Markets Report 2026, which surveyed 300 global LPs on their allocation priorities, found that DPI has risen to tie MOIC as the second most important metric in fund re-up decisions. Net IRR still leads. But the fact that LPs are now weighting realized returns as heavily as paper gains tells you everything about where the LP-GP relationship stands.

LPs are not waiting quietly. Secondaries transaction volume reached $240 billion in 2025, a 48% increase year-over-year and an all-time record. That volume does not appear because LPs are optimistic. It appears because LPs need liquidity that their GPs have not provided, and they are selling positions in the secondary market to get it.

GP-led continuation vehicles tell a parallel story. Volume grew from $35 billion in 2020 to $115 billion in 2025, up 62% year-over-year. LPs have been explicit in surveys about their tolerance: one continuation vehicle per GP per year is the maximum. Beyond that, it reads as delay rather than value creation.

The implications for fundraising are direct. GPs who demonstrate DPI momentum (actual cash returned to LPs) are winning in the current environment. Those who cannot show distributions are being cut from LP portfolios. The fundraising environment in 2025 was, by Bain’s assessment, “perhaps the most difficult the industry has ever seen.”

The sector rotation within PE deal activity reflects the pressure. Healthcare, technology, and energy infrastructure attracted a disproportionate share of 2025 deal value. Healthcare buyout deal value grew 45% year-over-year and 173% for deals over $500 million.

Watch the exit market in Q2 and Q3. That is where this resolves.

Sources: McKinsey Global Private Markets Report 2026 · Bain Global PE Report 2026 · CAIA: Continuation Vehicle Boom

Market Pulse

$904B in Deal Flow: Where Prediction Markets Say It Goes Next

$904B

Global buyout deal value 2025

28%

Kalshi recession odds, Apr 2026

+44%

Buyout deal value growth YoY

The headline number from 2025 is $904 billion in global buyout deal value, a 44% increase year-over-year and the second-best performance in industry history. Exit value hit $717 billion, up 47%. By almost any measure, PE deal activity recovered strongly last year.

The question is whether 2026 maintains that momentum, and the prediction markets are mixed on the answer.

Kalshi’s recession probability sits at 28% as of April 2026. It briefly hit 37% before pulling back, a spike driven by Iran conflict escalation, oil price pressure, and choppy macro data. Polymarket traders are pricing US recession by year-end at 30%. These are meaningful odds, not doomsday numbers, but high enough to shape how sponsors approach deployment.

The employment data complicates the story in the right direction: March nonfarm payrolls came in at 178,000 against a 59,000 expectation. Unemployment sits at 4.3%. The soft-landing case is alive. The recession case has not closed.

For deal flow, this translates to a bifurcated market. Sectors with structural tailwinds independent of macro conditions continue to attract capital. Healthcare buyout deal value grew 173% for transactions above $500 million in 2025. Cybersecurity is consolidating rapidly around identity, authentication, and governance. AI infrastructure and energy supporting it are drawing capital for reasons that go beyond standard PE return profiles.

The tariff picture adds another layer of complexity. Partners Group’s official assessment puts tariff exposure at a 1–3% EBITDA reduction on NAV-weighted basis for its portfolio. Manufacturers with global supply chains face headwinds above 10%.

For the next 90 days: secondary transaction flow stays elevated as LPs continue seeking liquidity. The $1.3 trillion in dry powder from 2022–23 vintages needs to deploy before fund timelines force difficult conversations. Platform buyouts (expected to represent at least 25% of total PE deal activity in 2026 per PwC) are the primary vehicle for that deployment.

Stay long structural, stay cautious on macro-sensitive.

Sources: Bain Global PE Report 2026 · Kalshi · Polymarket · PwC PE Outlook 2026

Blueprint Corner

AI Is a PE Value Creation Mandate. Your Data Infrastructure Decides Whether You Capture It.

2x ROIC

PE-backed companies that systematically deploy AI across functions generate nearly twice the return on invested capital compared to those that don’t. (FTI & Deloitte, 2026)

Accenture’s 2026 analysis calls agentic AI a “redefinition of private equity itself,” not an incremental improvement. FTI’s 2026 PE AI Radar identifies operating partners with AI integration expertise as essential rather than optional. These are not technology consultants overhyping their services. These are the data points GP executives are reading in their quarterly reviews.

Here is the part that gets skipped in most AI-and-PE conversations: the companies generating 2x ROIC from AI are not the ones that deployed the best models. They are the ones with the data infrastructure capable of feeding those models reliably.

AI does not run on strategy decks. It runs on data, specifically data that is clean, integrated, governed, and accessible across the functions where AI is supposed to generate value. A portfolio company with fragmented ERP systems, siloed customer data, and no consistent data definitions cannot extract AI-driven ROIC gains regardless of the model stack their operating partners select. The data problem swallows the AI investment.

This is where the value creation equation actually breaks down for most PE portfolios. The bottleneck is not the AI. It is the data plumbing underneath it.

For PE operating partners, the diagnostic question is direct: can your portfolio company’s data systems support the AI workflows you want to deploy? If the answer requires a long explanation involving legacy systems, manual reconciliation, and “we’re working on it,” the AI value creation timeline slides accordingly.

The companies that will generate 2x ROIC from AI in the next 24 months are building that data foundation now. Fast, integrated data pipelines. Governed data estates with clear ownership. Analytics infrastructure that delivers trustworthy outputs in deployment cycles measured in weeks, not years.

Blue Orange Digital works with PE-backed portfolio companies at exactly this layer: the data engineering foundation that makes AI operational rather than aspirational.

We build the pipelines, integrations, and governance frameworks that let your AI investments actually compound.

Sources: FTI 2026 PE AI Radar · Accenture · Deloitte

Blue Orange Digital

Data Engineering & AI for PE-Backed Portfolio Companies

You’re receiving this because you subscribed to the PE Value Creation Newsletter. To unsubscribe, click the link in your email client.